VA Loan Myths vs. 2026 Reality: Why “Zero Down” is Just the Beginning

As a Marine Veteran and Broker, I hear the same myths about VA loans every single week. “They take too long to close,” “The appraisals are too tough,” or “Sellers hate them.” In the 2026 DFW market, these misconceptions are costing veterans thousands and making sellers miss out on some of the strongest buyers available.

Let’s set the record straight on what a VA loan actually looks like today.

Myth #1: VA Loans Have a “Max” Limit

Reality: For 2026, the standard conforming limit has jumped to $832,750. But here’s the kicker: if you have your full entitlement, there technically is no loan limit. As long as you qualify and the appraisal supports the value, you can go well beyond that $832k mark with zero down payment.

Myth #2: The Appraisal is a “Deal Killer”

Reality: VA appraisals aren’t “tougher” than conventional ones; they’re just more focused on Safety, Soundness, and Sanitation. The VA wants to ensure you aren’t buying a money pit. In 2026, VA appraisal timelines in Texas are highly competitive, usually coming back within 7-10 business days. Plus, the VA “Tidewater” initiative actually gives us a chance to provide comps if an appraisal comes in low—something conventional loans don’t offer.

Myth #3: Sellers Have to Pay All Your Closing Costs

Reality: This is a huge one. Sellers can contribute up to 4% in concessions (which can cover things like your funding fee or even paying off a credit card), but they are not required to pay a dime of your closing costs. In a balanced market like we have now in Aledo and Weatherford, everything is negotiable.

Myth #4: You Can Only Use Your Benefit Once

Reality: Your VA benefit is for life. You can use it, pay it off (or sell the home), and use it again and again. In some cases, you can even have two VA loans at the same time if you have remaining entitlement.

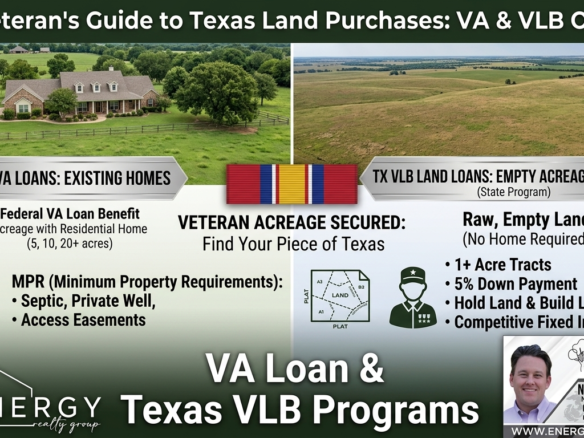

Texas Veteran Bonus: The VLB

Don’t forget that as a Texas Veteran, you also have access to the Texas Veterans Land Board (VLB), which can offer even lower interest rates for those with a 30% or greater disability rating.

The Bottom Line: If you’re a veteran in North Texas, you earned this benefit. Don’t let outdated myths stop you from building wealth through real estate. Whether it’s a ranch in Parker County or a home in Fort Worth, I’m here to make sure your offer gets accepted and your loan gets closed.

Join The Discussion