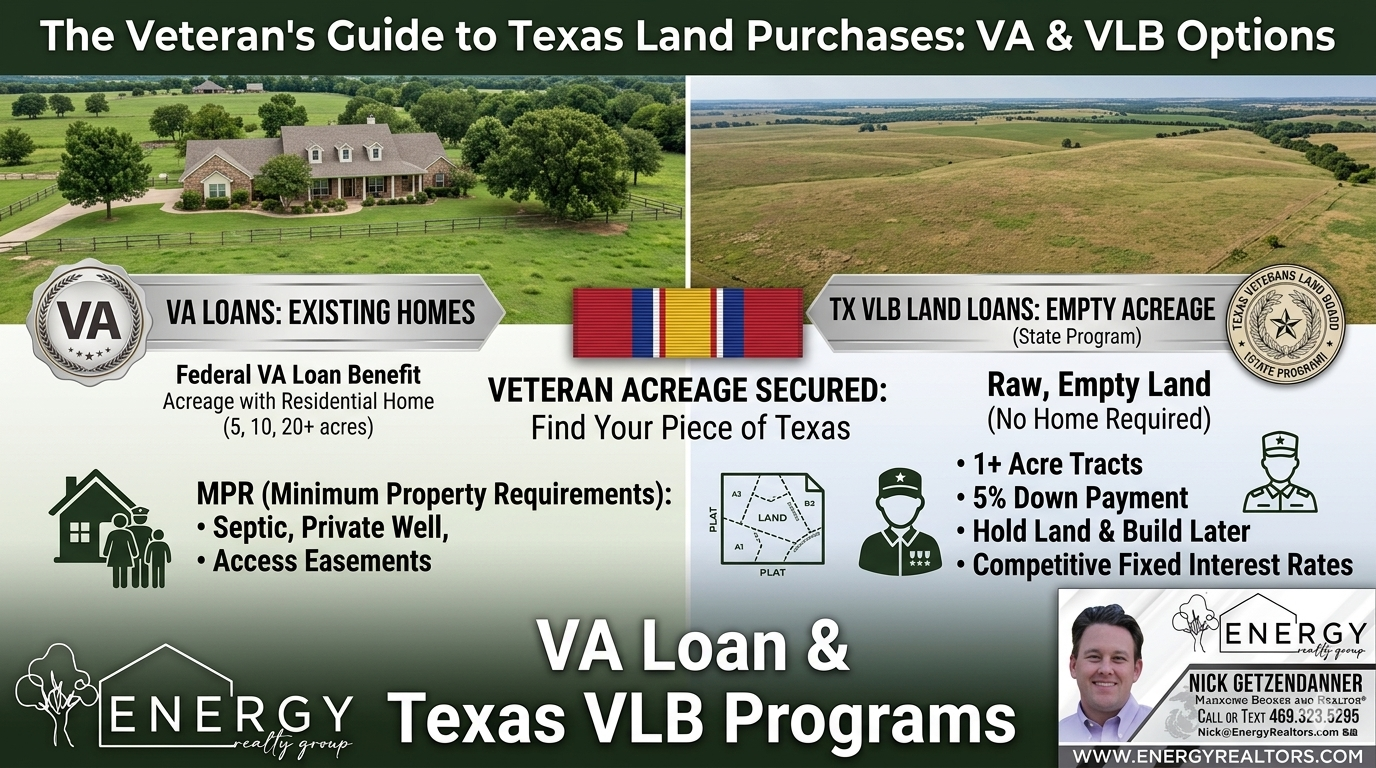

There is nothing quite like the feeling of owning a slice of Texas country. Whether your dream is a few acres in Aledo for your family to spread out, a horse property in Weatherford, or a quiet homestead out near Granbury, veterans frequently ask me the exact same question: “Can I actually use my VA loan benefits to buy land or acreage in Texas?”

The short answer is yes, absolutely—but there is a massive catch that catches many military buyers off guard. The VA will not lend on a raw, vacant piece of dirt just because you plan to build on it someday down the road. To utilize your hard-earned benefits, the loan must be attached to a residential property.

As a local real estate broker, mortgage professional, and Marine veteran, I specialize in navigating the intersecting worlds of rural land dynamics and VA lending regulations. Let’s bypass the textbook definitions and jump straight into the real-world operational rules you need to know to secure your Texas acreage homestead.

Rule 1: The Land Must Support a Home

To use a standard purchase loan through the U.S. Department of Veterans Affairs (VA) on acreage, the property must feature an existing residential home, or you must use a specialized VA construction loan to build a home immediately. If there is already a house on the property, the VA places no official limit on the number of acres the property can have. If you find a home sitting on 5, 10, or 20 acres out in Parker or Hood County, you can absolutely purchase it using your 0% down VA benefit, provided the appraisal supports the market value.

However, keep this under advisement: the VA loan is strictly a residential benefit. The value of the property must primarily come from the residential home, not from commercial farming operations, commercial livestock setups, or multi-unit income tracts.

The Raw Land Alternative: The Texas Veterans Land Board (VLB)

What if you do just want to buy a raw, beautiful piece of empty Texas acreage now and hold onto it until you are ready to build years down the road? Since a standard VA loan won’t cover vacant land, Texas veterans have an incredible, exclusive alternative: the Texas Veterans Land Board (VLB).

The VLB Land Loan program is completely separate from federal VA home loans and is financed directly by the State of Texas. Here is how it works for raw acreage:

- The Requirements: The tract must be at least one acre, have a minimum five-percent down payment, and be located entirely within the state of Texas.

- The Flexibility: Unlike federal rules, there is no requirement to build a home immediately. You can use the land for recreation, hunting, or future retirement planning while locking in highly competitive, below-market interest rates available only to Texas veterans.

Rule 2: The “Minimum Property Requirements” (MPRs) for Rural Land

When you buy a suburban tract home in Fort Worth, the federal appraisal process is relatively straightforward. But when you move out to rural acreage with an existing home, the VA’s Minimum Property Requirements (MPRs) become the primary hurdle. The VA wants to ensure the home is safe, sound, and sanitary from day one. When shopping for land, you must verify the following utility and access parameters:

- Access and Roads: The property must have direct access from a public road or a permanent, recorded private easement. If the home is on a private dirt or gravel road, the VA typically requires a documented joint maintenance agreement signed by the neighboring homeowners.

- Water and Utilities: Many Texas acreage properties rely on private water wells rather than city water. The VA allows this, but the well must pass a strict water quality and flow-rate test during the appraisal process.

- Wastewater Systems: Instead of a city sewer line, country homes utilize private septic systems. The VA appraiser will require a professional septic inspection to verify the system functions correctly and is completely free of surface pooling or mechanical failures.

Rule 3: Beware the Appraiser’s “Comparable Sales” Game

The number one reason VA acreage deals fall apart in underwriting is due to a lack of comparable sales data. Real estate valuations are entirely based on what similar properties have sold for nearby.

If you are trying to buy a custom home on 15 acres in a highly rural pocket, the appraiser must find recent sales of other homes on similar acreage within a reasonable geographic radius. If the closest match is 30 miles away, underwriting will flag the file. Working with an experienced local area broker ensures we analyze these micro-market data points before you submit an offer, protecting your earnest money from the start.

How Your Combined Broker & Mortgage Advantage Works for You

Navigating a VA loan or a Texas VLB land loan on an acreage homestead requires a highly coordinated strategy. If your real estate agent doesn’t understand rural septic rules, or if your loan officer doesn’t understand VA land appraisal guidelines, your deal can quickly stall out in underwriting.

Because I manage both the real estate side and the mortgage side of your transaction under one roof, we eliminate that breakdown in communication. I look at every property through a dual lens: evaluating the market layout as your REALTOR® while simultaneously underwriting the structural criteria as your lender.

If you are ready to find your piece of Texas, let’s get to work. Whether you are searching for existing country properties or need to explore land options using your military benefits, I’ve got your six. Contact me today to map out your strategy.

Join The Discussion