Let’s look at the critical realities of multi-parcel properties, how mortgage guidelines handle adjacent acreage in 2026, and the hidden traps you must avoid before signing on the dotted line.

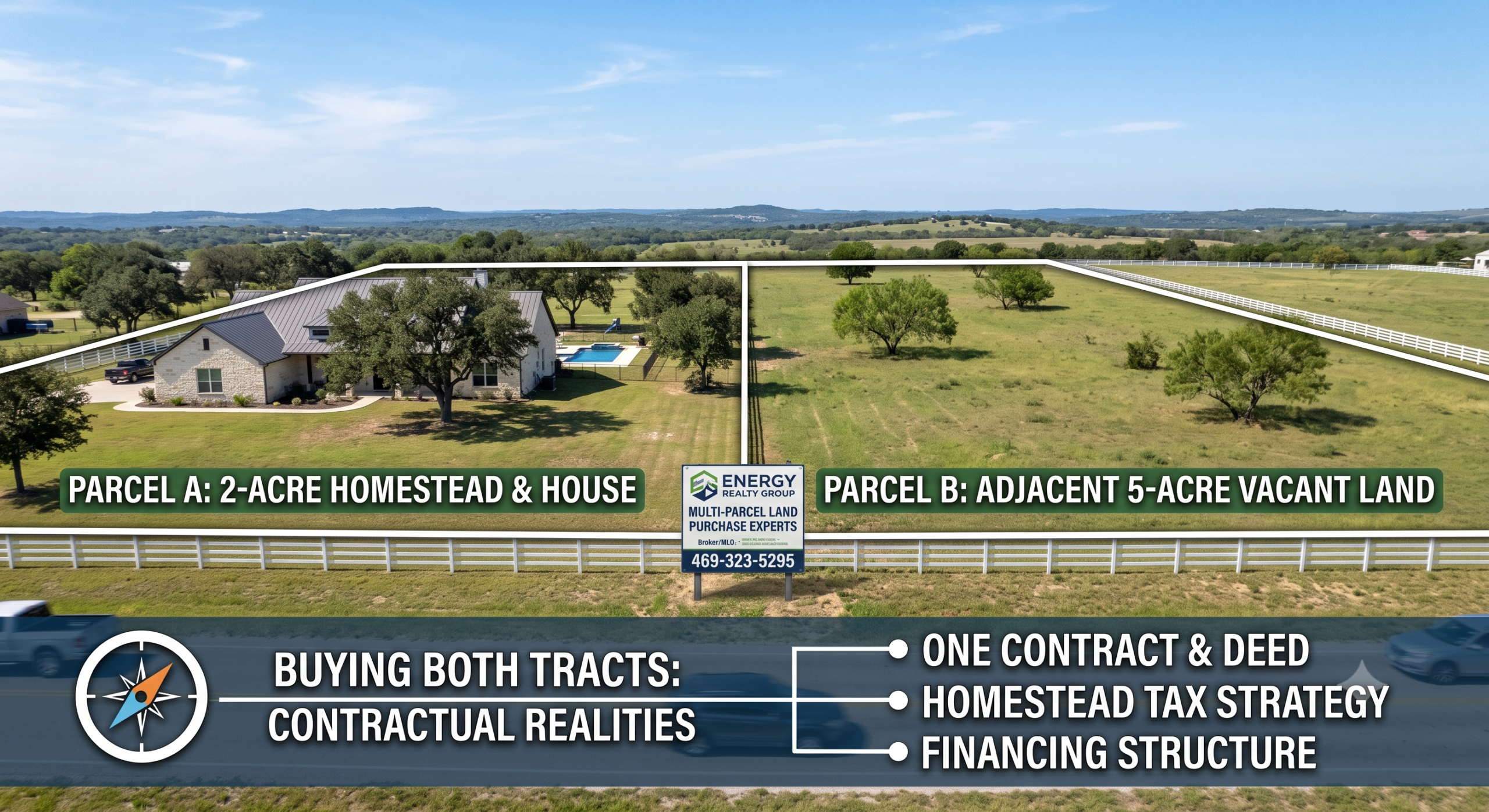

1. What Exactly is a Multi-Parcel Property?

In the real estate world, a “parcel” is a specific tract of land defined by the county appraisal district with its own unique legal description and tax ID number. A multi-parcel property simply means a single transaction that includes two or more separate legal parcels being sold together.

Crucially, just because a fence runs around both pieces of dirt and the same person owns them doesn’t mean they are legally tied together. They are distinct assets in the eyes of the county, the tax authorities, and most importantly, your mortgage underwriter.

2. Can You Finance a House and Adjacent Land on One Mortgage?

The short answer is **yes, absolutely**—but only if you follow very specific lending rules. Both standard conventional guidelines and VA loan protocols allow for multi-parcel financing under one mortgage file, provided the properties meet these three criteria:

- Contiguous Boundaries: The parcels must be physically touching. They can’t be separated by a public road, a distinct piece of land owned by someone else, or a major county easement.

- Single Ownership: Both parcels must be owned by the exact same seller, and both must be fully transferred to you simultaneously on the exact same deed at closing.

- The Highest and Best Use Rule: The appraiser must verify that the adjacent parcel acts as an extension of your primary residential yard/homestead. If the vacant adjacent lot has a separate zoning structure that allows for full commercial business operations, a standard residential mortgage underwriter will reject the file.

3. The Hidden Traps: Tax Rates and Future Legal Splits

If you don’t map out your multi-parcel purchase strategically from day one, you could face two major surprises after you move in:

The Tax Shock: Your primary homestead exemption will automatically protect the parcel that your physical house sits on. However, the county may not automatically apply that tax break to the adjacent vacant parcel. If that second piece of land was holding an agricultural exemption that you accidentally break by changing its usage, your tax bill can spike dramatically overnight.

The “One-Way Street” Platting Trap: When you wrap two separate parcels into a single mortgage, the bank places a lien on *both* pieces of land. If five years down the road you decide you want to sell off that extra 5-acre lot to a builder, you cannot simply sell it. You have to request a partial release of lien from your mortgage lender—a tedious, document-heavy process that requires a brand new appraisal and strict equity calculations.

The Broker-MLO Execution Plan

Navigating a multi-parcel deal requires an expert who can read county plat maps, cross-reference deed records, and directly write the mortgage file concurrently.

Because I manage both your real estate representation and your mortgage underwriting, we make sure the purchase contract explicitly calls out every single parcel ID, the title commitment binds them correctly, and the appraiser values the secondary tract accurately on day one. We eliminate the risk of a late-stage underwriter rejection, saving your deal and protecting your earnest money.

Secure Your Texas Footprint Legally and Safely

Buying the lot next door is the ultimate way to protect your perimeter and expand your lifestyle, but it demands precise contractual execution.

Eyeing a Property with Multiple Parcels?

Before you submit an offer, let’s look at the county plat lines, evaluate the tax implications, and verify that your mortgage structure will support both pieces of land seamlessly under one low-rate file. Contact me today to review your land scenario.

Join The Discussion