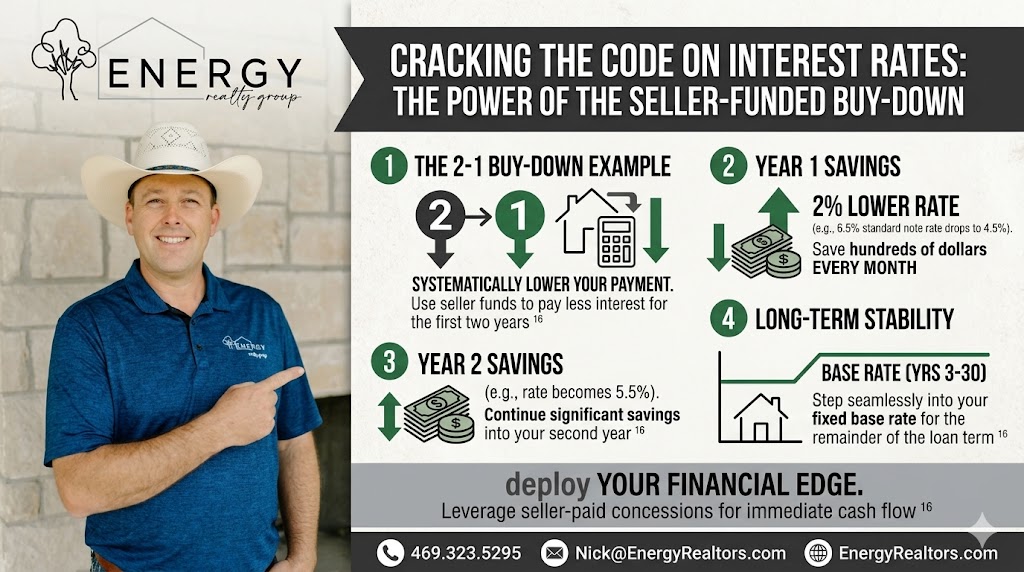

It’s called a seller paid interest rate buydown, and it is the single most effective financial tool available in today’s balanced housing market.

What is a Temporary Seller-Funded Buy-Down?

A temporary buy-down allows you to utilize seller concessions at closing to systematically lower your effective interest rate for the first few years of your mortgage. Instead of asking a seller for a traditional $10,000 or $15,000 reduction in the purchase price, we structure the contract so that the seller pays that money directly to your lender upfront to subsidize your monthly payment.

The money sits in a secure escrow account and is used to pay a portion of your monthly interest bill for you. You get a massively reduced payment, the seller gets their home sold without taking a major headline price cut, and your out-of-pocket costs remain completely manageable.

How the Math Works: The 2-1 Buy-Down Breakdown

The most popular structure in our market right now is the 2-1 buy-down. Here is exactly how it alters your financial landscape:

- Year 1: Your mortgage interest rate is reduced by a full 2% lower than your note rate. If your base market rate is 6.5%, you only pay an effective rate of 4.5% for the first twelve months. This can save you hundreds of dollars every single month.

- Year 2: Your rate bumps up slightly to 1% lower than your note rate (an effective 5.5% in this scenario), keeping your savings alive for another full year.

- Years 3 through 30: Your payment steps up smoothly to your standard note rate of 6.5% for the remainder of the loan term.

Why This Wins Over a Simple Price Cut

A lot of folks assume that cutting $15,000 off the purchase price of a $500,000 home is the best way to save money. But a $15,000 price drop only shaves roughly $90 a month off your standard payment.

If you take that same $15,000 as a seller concession and deploy it into a 2-1 interest rate buy-down instead, your monthly savings during the first year can easily exceed $400 a month. That is immediate, structural cash flow that stays in your pocket right when you need it most—while you’re setting up your new household.

The Refinance Safety Valve: Here is the best part of this strategy: if macro interest rates drop significantly at any point during those first two years, you can refinance into a permanent lower rate immediately. Any remaining funds sitting in your seller-paid buy-down escrow account aren’t lost—they are automatically applied directly to your principal balance reduction. You lose absolutely nothing.

Deploy Your Financial Edge

Winning in real estate isn’t just about finding the right house; it’s about engineering the right financing structure. Because I quarterback both your real estate strategy and your mortgage lending, we can build custom buy-down terms directly into your purchase contract seamlessly. If you are ready to stop letting macro interest rates dictate your lifestyle, let’s connect. I’ve got your six.

Join The Discussion