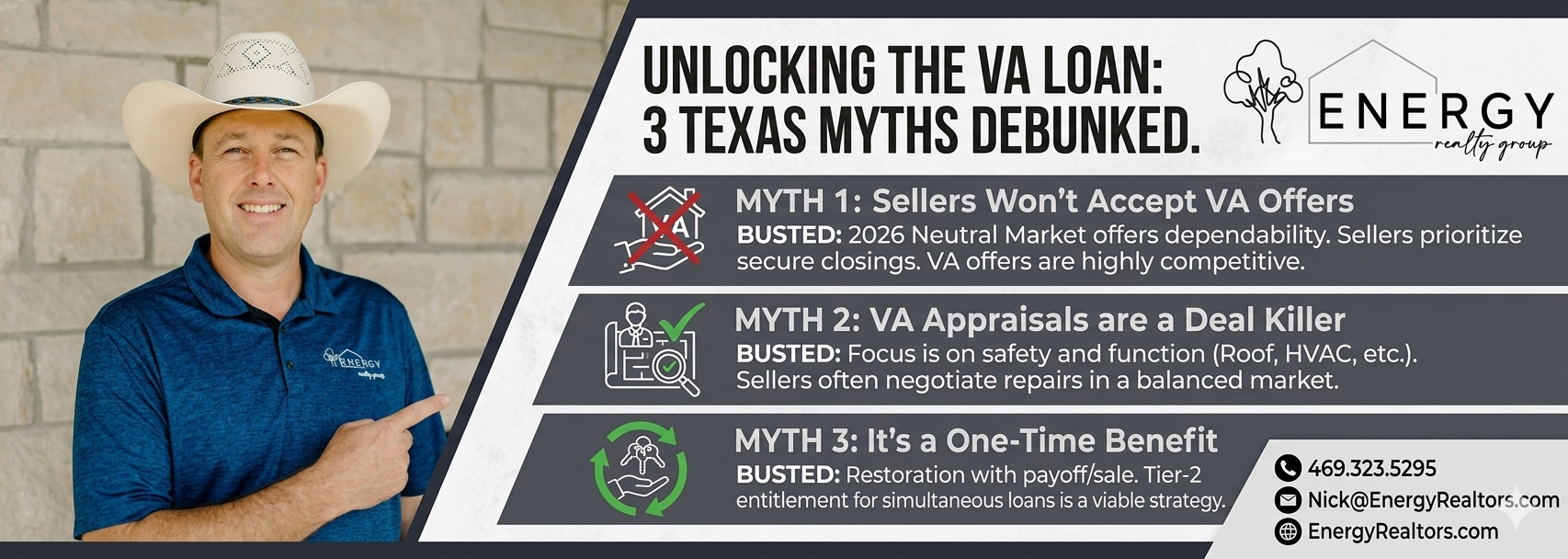

Myth 1: “Sellers Won’t Accept VA Offers in Today’s Market”

A few years ago, when sellers were getting thirty cash offers over asking price in twenty minutes, VA loans had a reputation for being pushed to the back of the line. But this is 2026. With average days on market hovering around 55 days in Fort Worth, the power dynamic has leveled out.

Sellers are looking for solid, qualified buyers who are guaranteed to make it to the closing table. Because VA loans are backed by the federal government, they represent incredibly secure financing. When packaged and presented correctly by a broker who speaks the language, a VA offer is highly attractive to a seller looking for a dependable closing.

Myth 2: “The VA Appraisal Process is a Deal Killer”

Many folks believe that VA appraisers are hyper-strict nitpickers looking to tank a sale over minor aesthetic flaws. In reality, the VA’s Minimum Property Requirements (MPRs) are simply in place to ensure the home is safe, sound, and sanitary for you and your family.

They are looking at the big structural items: a solid roof, functioning HVAC systems, clean water, and a lack of wood-destroying insects. In a balanced market, if an issue does pop up on an appraisal, sellers are highly motivated to negotiate repairs or offer concessions to keep the deal moving forward. It’s no longer a “take it or leave it” environment.

Myth 3: “You Can Only Use Your VA Loan Benefit Once”

This is one of the most common pieces of misinformation out there. Your VA loan eligibility is not a one-and-done coupon. It is a lifetime benefit that restores itself once your previous loan is paid off (like when you sell your previous home).

Even better? It is entirely possible to have tier-2 (second) entitlement, which allows you to hold two VA loans simultaneously under the right structural conditions. If you are looking to move up to a larger home in Aledo or Granbury but want to keep your first home as an income-producing rental property, your VA benefit can often help you make that happen.

Why It Matters Now: In a neutral market, you can combine your 0% down VA loan benefit with negotiated seller concessions. This means you can ask the seller to pay down your interest rate temporarily or cover your closing costs entirely—allowing you to keep your hard-earned capital in your bank account.

I’ve Got Your Six

Navigating the real estate landscape requires a clear strategy and a team you can trust[cite: 3]. Whether you are hunting for acreage in Parker County or trying to maximize your military benefits in Fort Worth, I am here to ensure you win the mission[cite: 3].

Join The Discussion